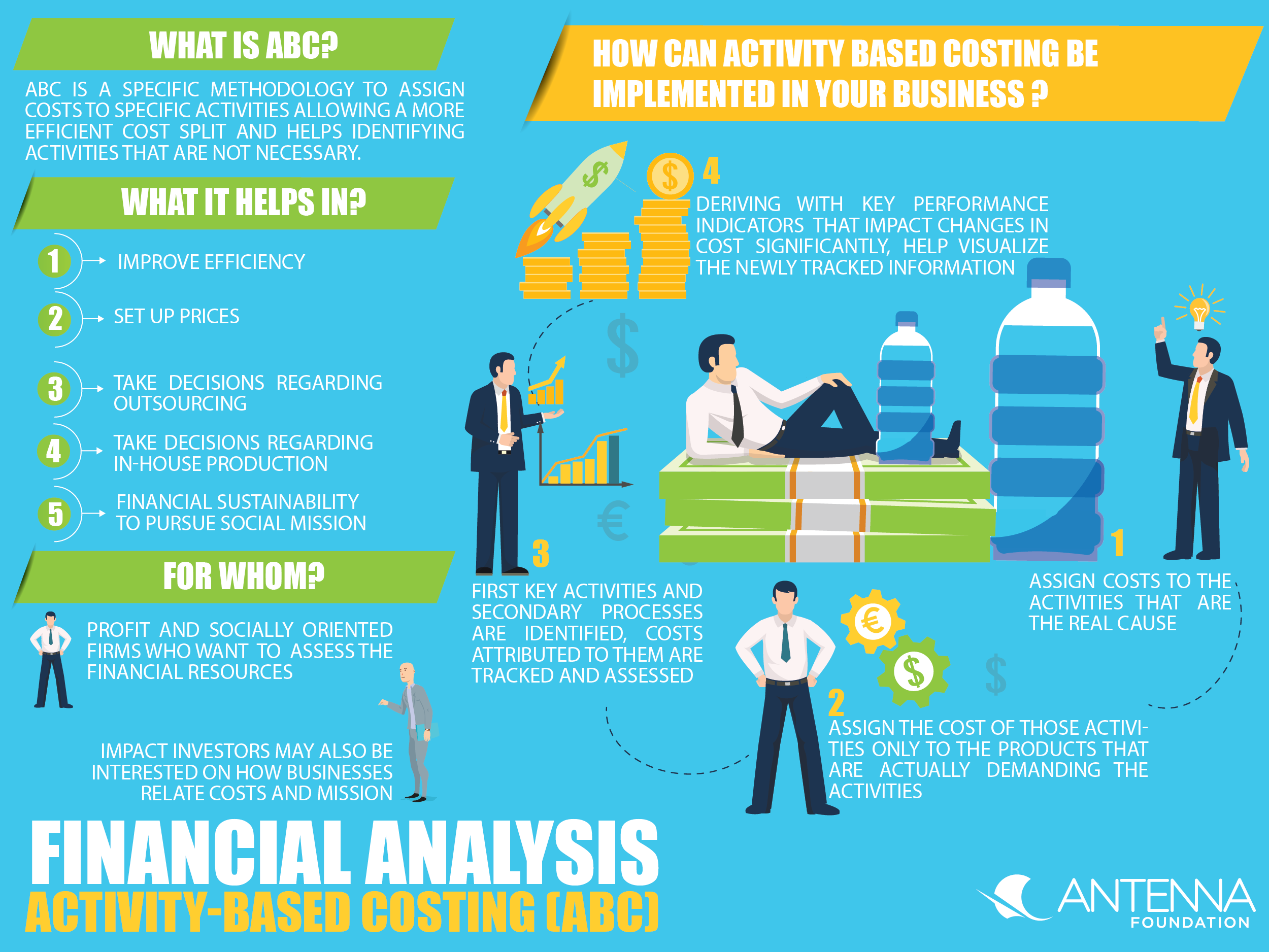

Executive Summary

Financial analysis allows a company to overview its costs and identifies potential cost positions that could be lowered to become more effective per money invested. Activity-based costing (ABC) is a specific methodology to assign costs to specific activities allowing a more efficient cost split and helps identifying activities that are not necessary. Thoroughly applied it will lead to potential cost reduction and can help increase profit per unit produced.

This factsheet provides the reader with an introduction to activity-based costing. This method allows the implementer to define costs per activity from developing, sourcing, producing and delivering a product or service.

The case study on Oromo Self Help Group (OSHO) in Ethiopia provides the reader with insights on how important it was for the NGO to clearly identify costs of production and service offering of fluoride removal filters for the local market in order to create a sustainable model.

What is financial analysis about?

Financial analysis allows a company to overview its financials. Financial analysis can be executed in various ways and to different extent. In our specific case we focus on costs to identify different cost positions of a safe water enterprise that could be lowered to become more effective per money invested. For safe water businesses it is important to know the costs of its specific activities (manufacturing, sourcing, sales, marketing etc.). Traditional costing systems assume that products cause costs. There is also a different approach so-called activity-based costing (ABC). ABC systems have activities as the fundamental cost object. But the system is flexible enough to relate costs to customers, processors, management responsibility and not just products. Activity-based costing assigns for example manufacturing overhead costs to products or services in a more logical manner than the traditional approach of simply allocating costs on the basis of machine hours. This approach can facilitate safe water companies to clearly identify the cost positions related to different products, services and activities within the company. It will help taking decisions how to improve its efficiency, set prices and take decisions regarding outsourcing or in-house production etc. (SCHMIDT, 2017; FINANCIAL SUPPORT, 2009).

Why is financial analysis important?

The primary financial goal of a standard business is profitability. A safe water enterprise may have profitability as its goal, or it may not. For instance, the goal may be to be financially sustainable so that sales revenue covers both your standard business costs and the extra costs you incur to pursue your social, environmental and/or cultural mission (we refer to these as “social costs”). In this case, your goal is to have no funding support. As a social enterprise, it is important to be clear about your financial goals, and to interpret your financial statements accordingly. In achieving profitability a major focus of safe water enterprises lies in managing its various costs. This requires accurate and timely financial and operational performance data to inform decision-making about enterprise operations and growth. A clear accounting of the costs aside from social impacts and profitability of enterprises is critical to demonstrating the value of social enterprise in communities and to make a case for investment and support from government and private sector investors. For example, it can be easier to fundraise when you can clearly describe the costs that relate to your social/environmental mission. Activity-based costing in particular can inform a company to identify and adapt (or even eliminate) products, services or processes to increase social and financial performance (GOSSLIN, 2006).

For whom is activity-based costing useful?

ABC is interesting for profit and socially oriented firms who are starting out their business and therefore must assess the financial resources required. But it is of special interest for social enterprises in their first years, where costs should be thoroughly monitored and assessed in regard to effectivity.

Impact investors may also be interested in acquiring insights on how safe water businesses can concretely relate costs and mission through ABC.

Subscribe here to the new Sanitation and Water Entrepreneurship Pact (SWEP) newsletter. SWEP is a network of organizations joining hands to help entrepreneurs design and develop lasting water and sanitation businesses.

How can activity based costing be implemented in your business?

Costs are collected for each activity as an independent cost object. Therefore:

- Assign costs to the activities that are the real cause

- Assign the cost of those activities only to the products that are actually demanding the activities.

- First key activities and secondary processes are identified. Costs attributed to them are tracked and assessed.

- Deriving with key performance indicators for the processes that impact changes in cost significantly, which help visualized the newly tracked information.

Specific tools to help implementing ABC can be found subsequently:

- Tools are available online, for example under FSG & CF INSIGHTS (2012)

- Simple explanation of cost accounting for social enterprises

- Simple explanation of basic financial tools and ratios

- Financial viability check and automated ratio tool

The case study of OSHO in Ethiopia provides insights on how ABC has been implemented in a safe water project and highlights its positive outcomes.

Activity-Based Costing Toolkit

Activity Based Costing (ABC) and Traditional Costing Systems

Activity Based Costing ABC, and ABC Management Explained - Definition, Meaning, and Example Calculations

A Review of Activity-Based Costing: Technique, Implementation, and Consequences

Easing the Transition to Commercial Finance for Sustainable Water and Sanitation

This publication discusses different options of how sustainable water supply and sanitation services in developing can be funded and makes propositions how the existing funding gap can be met. Different financial frameworks are explored and presented.

GOKU, A. TRÉMOLET, S. KOLKERR, J. KINGDOM, B. Easing the Transition to Commercial Finance for Sustainable Water and Sanitation. Washington, DC: World Bank URL [Accessed: 18.04.2018] PDF